2020 was a watershed year in large deals in engineering services. The large deal momentum continued in 2021 as well, though at a slower pace than in 2020. I found few differences in large deals in 2021 vs. 2020 (based on the deals I am aware of)

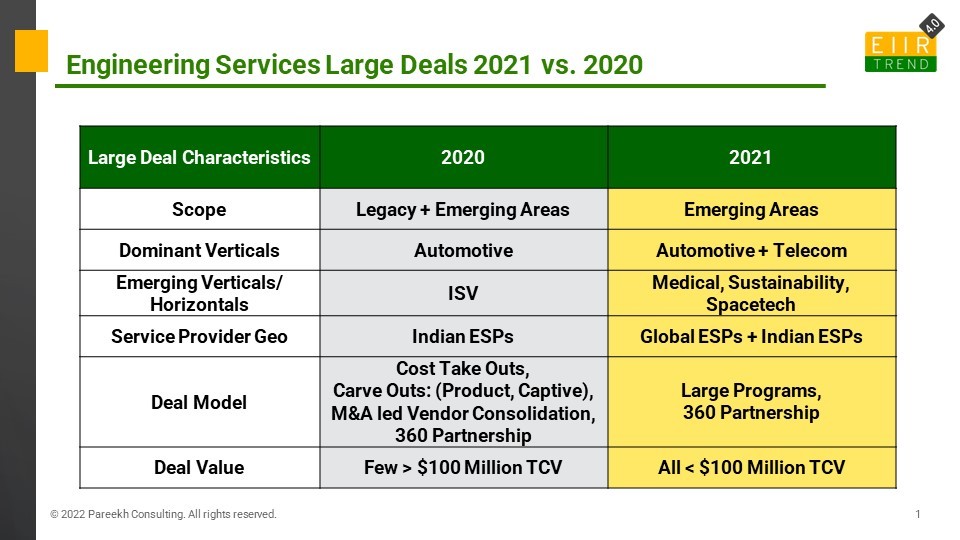

- Scope: In 2020, deals were from both legacy areas and emerging areas, while in 2021, almost all deals were from emerging areas.

- Dominant Verticals: In 2020, automotive was the dominant vertical for large deals though there were deals from other verticals also, including aerospace, oil & gas, etc. In 2021 automotive and telecom verticals stand out. Automotive continues to dominate large deals (Read here), while telecom deals can be attributed to 5G pickup.

- Emerging Verticals/ Horizontals: In 2020 emerging vertical was ISV, and in 2021 we see deals from medical software, new age sustainability firm, space tech, among others.

- Service Providers Geography: In 2020, all large deals in the public domain were from Indian Engineering Service Providers. While in 2021, large deals of Global Engineering Service Providers are also visible.

- Business Model: In 2020, the business models of the majority of large deals were related to cost take-outs, including carve-outs of captives and products. There were examples of enterprise restructuring due to M&As and also vendor consolidation. 360-degree partnerships with technology providers were also there. In 2021 large cost take-out or carve-out deals are absent. Now deals are parts of large programs and 360-degree partnerships.

- Deal Value: Deal values were very high in 2020 (by engineering services deal benchmarks), and few deals were even greater than $100 million. In contrast, in 2021, all deals are sub $100 million.

Bottom Line: The engineering services market is in transition. I believe an inflection point has reached, and enterprises are using engineering service providers for new areas large programs more than ever, and it is reflected in changes in the large deal landscape. Though mega deals are down but overall, we had the best quarter ever in engineering services from the growth perspective (Read here). That means a larger number of clients are engaging engineering service providers now with strategic programs. This is a good sign for the market where only 5% of spend is outsourced. Onwards and upwards engineering services!