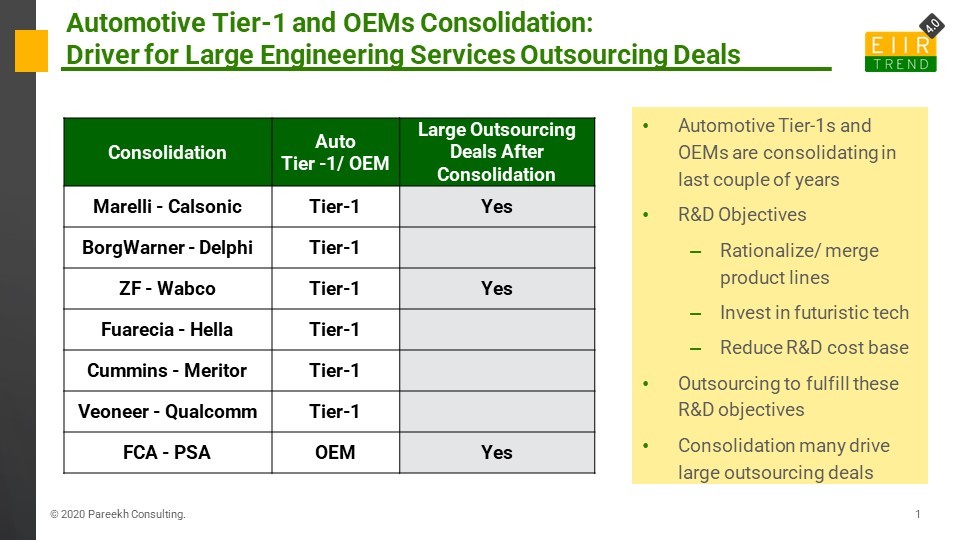

There is consolidation going on in the automotive industry among tier 1 – suppliers as well as among OEMs. This consolidation is becoming a driver for large engineering services outsourcing deals.

The above exhibit lists major consolidation exercises in the last couple of years and also mentions whether large deals followed the consolidation exercise. There were three such recent examples. There are a couple of more post-consolidation large engineering services deals in this set, but since information is not in the public domain, so I didn’t call them out.

One of the critical points in the automotive M&A business case is R&D rationalization. There are three ways for R&D rationalization post-consolidation:

- Rationalize/ merge product lines: Make decisions on different product lines. Overlapping product lines can be merged, or some can also be discontinued in the proper timeframe. Some product lines may be obsolete with changing technologies in the next few years. But discontinued and obsolete ones will need to be also supported for some time. Some of the support work for sunset product lines can be outsourced.

- Invest in futuristic tech. Consolidate futuristic tech projects and remove duplication among entities. Identify gaps and increase investment in priority areas, including both existing and new technologies. For example, if both entities are investing in EVs but not in Autonomous Driving, so merged entity can remove duplication in EVs and invest savings in Autonomous Driving. Engineering service providers can help scale up competencies in selected areas post-consolidation.

- Reduce R&D unit cost: Analyze the current per hour R&D cost base (both internal and external) and work out a revised reduced target per hour R&D cost. Reduce it by leveraging more work from emerging countries, including India, by leveraging various operating models. Investment in new technologies for engineering processes such as automation, virtualization, simulation, digital thread, digital twin, AI, VR, and AR can increase R&D productivity and decrease R&D unit cost.

Some engineering service providers can help automotive enterprises in all of the above. So even if overall, R&D spending of the combined entity might decrease as per the business case of M&A, there is a good chance that engineering outsourcing might increase.

All engineering service providers can’t capitalize on higher post-consolidation outsourcing opportunities. For this enterprise will select a few strategic partners. So for participating in this exercise, service providers need to ensure the following:

- Account Entry. Auto enterprises will most likely select their post-consolidation strategic partners from their current engineering service provider base. Any engineering service provider who is not incumbent will find it difficult to get a seat at the table. One way to get account entry is by acquiring a smaller service provider which is incumbent in that particular account.

- Domain Competency Development: Identifying which competencies are important and developing or strengthening offerings, be it EV, Battery, Autonomous Vehicles, ADAS, Connected Cars, Infotainment, etc. Wherever applicable, engineering service providers should invest in testing, labs, solutions, and accelerators to demonstrate their expertise. Solutions and accelerators help the service provider jumpstart delivery for a new engagement and help in working better and faster.

- Process Competency Development: Auto enterprises will be looking to leverage new technologies for process improvement. Technologies such as automation, virtualization, simulation, digital thread, digital twin AI, VR, and AR can increase R&D productivity and decrease R&D unit cost. Engineering service providers with work experience across multiple customers in multiple industries are in a unique position to become experts and knowledgeable about best practices for engineering process improvement.

- Business Models: Different business models might be required to participate in post-consolidation large deals. Depending upon client situation and deal construct, it may involve upfront cash payment, captive carve out, rebadging employees, and co-investment in futuristic tech, among others.

- Geographic Footprint: Important geographies for engineering work for auto enterprises are where their manufacturing and R&D centers are located and also, in some cases, where their customers or suppliers are located. Emerging countries are also important in reducing the overall R&D cost base. Even if the engineering service provider doesn’t have a current delivery base in desired locations, it should be ready to make the investment if the client requires it, as we have seen in a couple of recent deals.

- Talent Development: In times of great resignation and atrocious attrition, automotive talent availability is one of the most critical factors to give confidence to the client about delivery and scaleup capabaility. The ability to identify, recruit, train, and retain automotive-specific talent will be a competitive advantage

- Thought Leadership: In emerging engineering services areas, when there are not many proof points, thought leadership is the best way for an engineering service provider to articulate and demonstrate its value proposition and differentiate from other engineering service providers. Even if proof points are available, a good thought leadership artifact can often act as an attention catcher and a conversation starter.

Bottom line: Automotive has the highest share of engineering service outsourcing among all industry verticals. (Read here). Automotive consolidation further drives this sector. Proactive engineering service providers can capitalize on this trend by preparing themselves in advance. Whenever you hear about automotive consolidation, assume it as a piece of good news for automotive engineering outsourcing.